Updated: Feb 5, 2019

How the $20 Trillion National Debt Will Affect the Average American

Estimated read time: 15 minutes

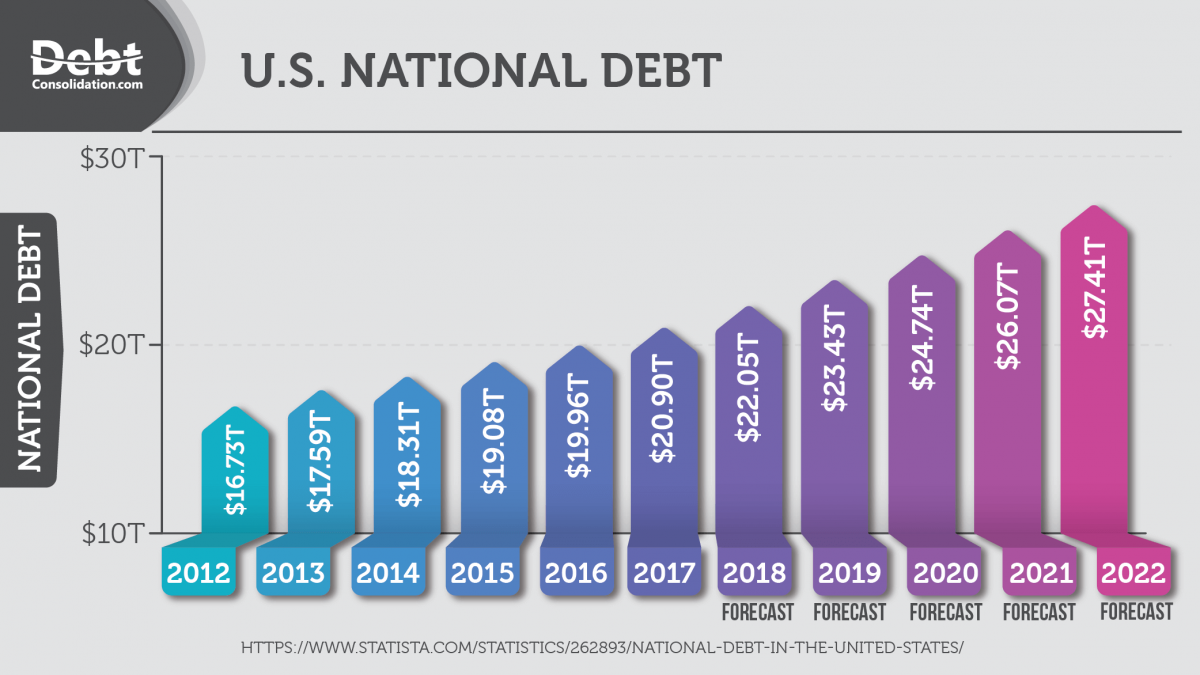

More than $20 trillion.

That’s how big the nation’s debt is—the highest it’s ever been in the history of the United States.

In fact, we’ve exceeded $20 trillion in national debt with a per capita debt of ~$60K.

Most people know what having personal debt means.

It means giving up that gorgeous blouse or looking away from that pair of shoes you’ve been eyeing.

Maybe it means fewer beers out with the guys or eating in instead of eating out at your favorite spot.

Basically, it means you’ve spent more than you make and you’ve got to curb corners somehow to avoid driving yourself into a deeper, more irreparable debt.

But what exactly does it mean when the nation is in debt?

What is the national debt and should it even matter to you?

Can that trillion dollar number ever even affect you?

Unfortunately, the answer is yes.

The national debt can and may impact you in your lifetime.

Because even if your personal finances are in order, you have to remember that you’re interlinked within a broader group of people.

You belong to a country whose influences and problems will eventually impact you.

Let’s take a look at how this debt can impact your wallet and why you should pay attention to your personal finances but also be aware of what’s going on around you.

National Debt Basics

What does it mean when the nation is in debt?

The nation is in debt.

That sounds alarming, but few people really know what it means.

Before we get into that though, I want to talk about the difference between a debt and a deficit.

Because often people confuse the meaning of these two terms or even use them interchangeably, so let’s start there.

A deficit is defined by the Merriam Webster dictionary as a "deficiency in amount or quality."

For our purposes, we’re talking about money, so a deficit means a shortage of funds.

A budget deficit is when the government spending equals more money than it brings in from the sources that help it generate income.

The main thing that the government depends on for that "income" is taxes.

These include things like individual, corporate, or excise taxes.

When you think of it in terms of a business operation, a deficit is when you’re spending more on business expenditures than you’re making in revenue.

For example, let’s say you have a bakery and you’re spending more money paying staff and buying ingredients to create your goods than you’re actually making in sales.

Then this would mean that you’re working in a deficit.

The federal or national debt, on the other hand, is simply the total accumulation of the federal government’s budget deficits.

In other words, the debt is the total money our government owes to its creditors.

Going back to our bakery example, a total of all the deficits or shortages of money the business is lacking is what causes it to accumulate debt.

Its debt is the amount of funds that it has to pay back to people, such as its vendors, suppliers, and even to banks.

Anyone that they may have taken a loan from to continue day-to-day operations.

How is it possible for the government to spend more than it has?

Most people understand how a person can come into debt by spending more money than they have.

For example, maxing out credit cards, borrowing loans, taking some money from a good friend or relative are all ways that you can end up spending more than you can actually afford.

But the matter becomes a little more complicated when the government is involved, because it doesn’t use the same resources you do to run up a debt.

So how does a government get the funds to spend more than it actually has?

As we talked about earlier, the government is heavily reliant on taxes to cover its spending.

But when the taxes aren’t enough to cover its payments, it has other resources it can turn to when it needs to borrow some funds.

To obtain the extra money it spends, the US Treasury Department issues instruments like treasury bills (T-bills), treasury notes (T-notes), and treasury bonds (T-bonds).

There are some key differences between each of these securities.

The primary difference is how long they take to mature.

T-bills. These are short-term debt obligations backed by the Treasury Department that mature in less than one year.

Typically, these are sold in denominations of $1,000, and the maximum purchase allowed is $5 million.

The government often uses the money made from selling T-bills to fund things like the construction of highways and public schools.

T-notes. These are debt securities and are primarily issued for terms of 2, 3, 5 and 10 years with a fixed interest rate.

You can get these from the government either through a competitive or non-competitive bid.

A competitive bid means that investors get to determine the yield they want.

The yield is the amount of return you get on an investment, expressed as a percentage rate.

The caveat is that their bid may or may not get approved.

With a non-competitive bid, the yield determined at the auction is what the investor accepts.

T-bonds. Like T-notes, these are also fixed-interest debt securities.

But the difference here is that they have the longest maturity term of the three options, usually more than 10 years and closer to 30 years.

T-bonds pay out interest semi-annually, and the income you make from them is taxed only at the federal level, not the state level.

Bonds are known to be risk-free because they’re issued by the government with only a very small risk of default.

By selling T-bill, T-notes, and T-bonds, the federal government is able to get the money it needs to provide government services and programs that its citizens depend on.

We’ll talk more in a bit about what those services are.

But for now, it’s important to understand that the government finances its deficit or shortage of funds by selling these securities.

It sells them to both domestic and foreign investors, corporations and other global governments.

The money that these individuals and companies pay for treasury securities is then used to fund government activities and programs.

Debt Distribution

Now that you know how it’s possible for the government to spend more than it has, you’re probably wondering exactly where did it spend all those funds

After all, $20 trillion is no small amount.

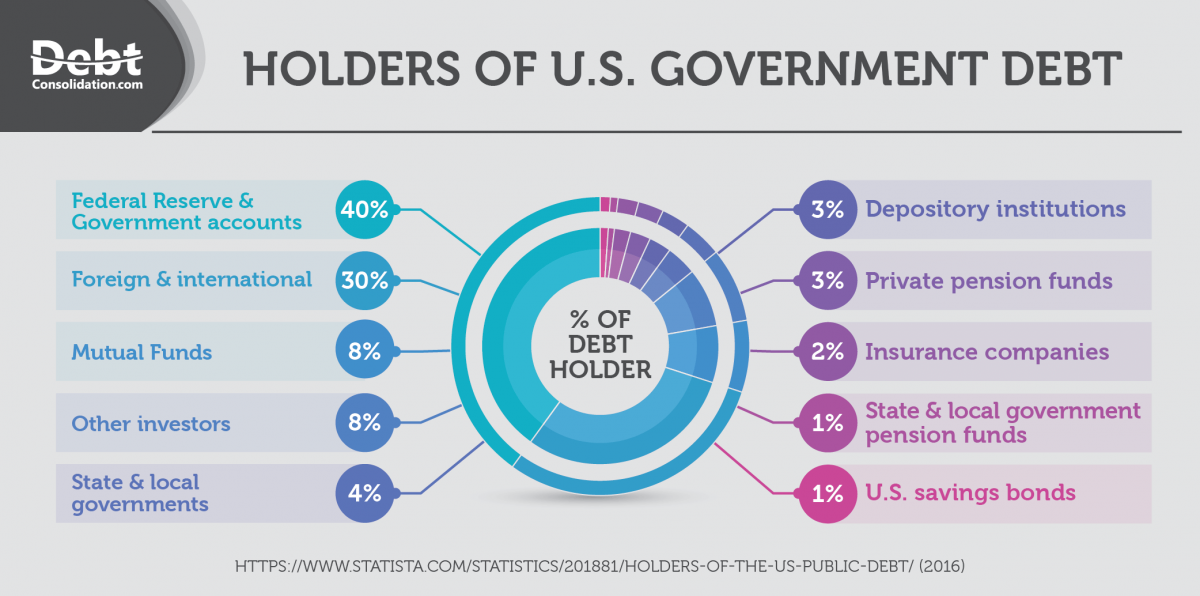

Think of the debt as being broken down in thirds.

Two-thirds of that debt is held by the public through money the government owes to buyers of the T-bills, T-notes, and T-bonds we talked about earlier.

The remaining one third is money the US government owes itself.

This is known as intragovernmental debt.

The money for this kind of debt is owed to the US departments that hold government account securities.

For instance, the Social Security Trust Fund is the government program that the government owes the greatest amount of debt to.

How is that even possible?

Look closely, and you’ll see that social security has been running on surpluses for a long time.

The government has optimized on those surpluses by using them to pay for other departments.

That’s why it owes money back so much money to the Social Security Trust Fund.

So the next time you’re asked who owns the US debt, you can confidently say that it’s owned by everyone who has retirement money with the government’s social security program.

Because that’s what the government has used to source its projects and spendings!

It’s kind of like borrowing from Peter to pay Paul.

Think about what would happen if you were to do something like that with your personal finances.

If you borrowed from one person to pay another, that wouldn’t diminish your debt.

It would only transfer it from one party to another.

And if you keep borrowing and borrowing with no end in sight, your debt will grow exponentially.

That’s why the US national debt is where it is.

In fact, it climbs an average of $3.8 billion a day.

Here’s another interesting statistic to put it into perspective: the government has to borrow about 41 cents of every dollar it spends.

That’s a big chunk of its spending!

Debt Growth

Debt can escalate, and it can often escalate fast; that’s what’s happened throughout the years with the US debt

Of course, when the debt started, it was nowhere near the trillion mark.

But many years of mismanagement and allowing the debt to fester and grow has brought us where we are today.

So what caused it to get so out of hand?

We can chalk it up to five main causes.

1. The government introduced several new programs that it didn’t have enough money to start.

To make matters even worse, it implemented tax cuts to benefit its citizens.

Remember, tax is where the government makes its money.

But with less taxes and more spending, it created a recipe for disaster and only exacerbated the national debt.

2. It borrowed from the Social Security Trust Fund.

This isn’t anything new.

In fact, many presidents have borrowed from Social Security, including Roosevelt, Bush and even Obama.

But the less money that’s in social security, the less money the government has to work off of when Baby Boomers retire.

As this generation starts hitting its retirement years even heavier, the government will have to issue them the retirement money they’ve rightfully earned.

This might mean that the government has to eventually increase taxes to help pay back into the social security fund.

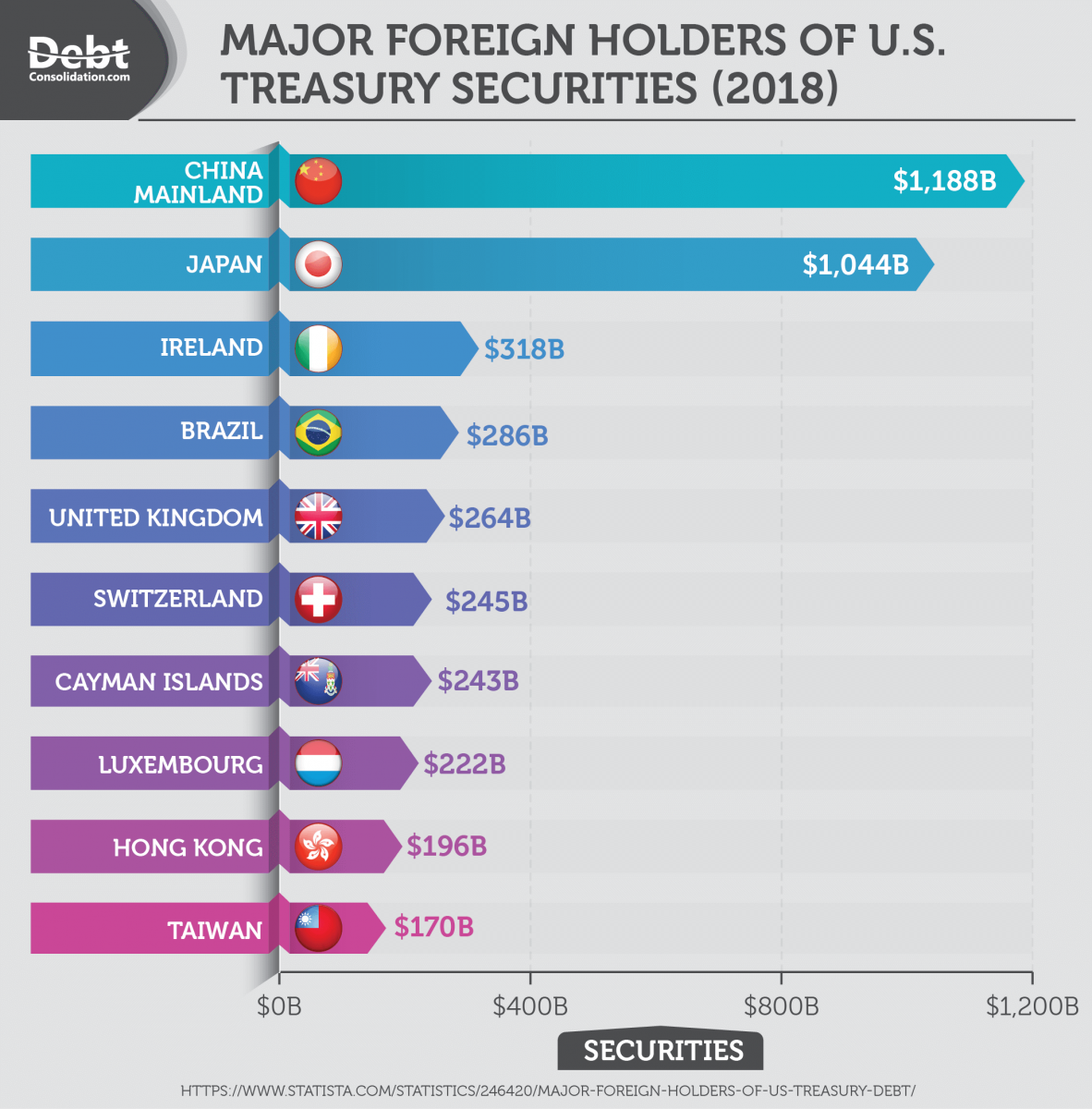

3. It borrowed from China and Japan.

In essence, China and Japan have bought the US debt by investing in our treasuries.

The more they put money in our treasuries, the more they weaken their own currencies against ours.

This made it cheaper and more appealing for the US to buy from them, keeping these countries profitable.

This serves as a "win-win" for everyone involved. Except that it also increases our debt.

4. Low tax rates have contributed to our debt, because low tax rates equal low tax collections.

And as we know, low taxes means less money for the government to use.

5. Congress keeps raising the debt ceiling, making it higher and higher and allowing for more and more debt.

The debt ceiling is the highest that Congress allows the debt to be.

As you might imagine, our trillions of dollars of debt didn’t happen overnight.

The nation’s debt isn’t new news by any means, but then why or how could any of this come to affect us as taxpayers and citizens?

Let’s talk about that now.

Impacts

How does the nation’s debt affect me?

For a long time, many of us have seen the nation operate under debt.

So for most of us, the nation’s debt is no greater than a number we occasionally toss around at each other and discuss on a whim.

Because we haven’t really seen the effects of this debt. Yet.

But that doesn’t mean we’ll be safe from its impact forever.

Say for example the people who hold the nation’s debt suddenly ask for a larger interest on the debt they hold, or they ask for the debt to be repaid.

Then what?

Like I said, that hasn’t happened yet, which is why many Americans aren’t privy to the effects that kind of a situation can have on us as consumers.

But if it ever were to happen, it would force the government to act. And act fast.

And when it does is when we’ll all see the impacts.

If, or when, this situation does arise, is when we’ll see several impacts to our day-to-day.

First, you’ll probably notice higher interest rates.

When the debt continues to rise, that means that investors and foreign governments will be less inclined to purchase Treasury bonds, causing interest rates to go up.

When interest rates rise, that means you’ll end up paying higher interest for your home, credit cards, auto and all other lending products.

Second, you might see a weaker job market.

When companies are faced with an increase in costs such as taxes, interest rates, etc., they won’t be as likely to hire.

In fact, they’ll be more inclined to layoff and cut back on jobs.

They’ll do anything to tighten up their purse strings, including cutting the salaries of even the highest paid executives of large corporations.

No one is safe from these cuts when the financial landscape starts looking bleak.

But when companies start cutting back like this, it means a weaker job market and fiercer competition for the good jobs out there.

You might want to think twice before quitting your current job, regardless of whether you love that job or not.

Third, you’ll see an increase in taxes.

The government cannot sustain the debt when there aren’t enough taxes coming in.

To manage the debt, therefore, the government will need to increase how much it takes in in taxes so that the nation can cover this debt.

The only other alternative to increasing taxes would be for the government to reduce spending drastically.

But historically, that’s proven difficult to do.

If the government is forced to cut back on spending, that means it will have to reduce benefits and programs.

This will affect programs like Social Security, Medicare, and student financial aid, which will have to be significantly reduced.

Based on what has happened in the past, it’s more probable that taxes will be increased, which means everyone will be forced to pay higher taxes, eventually.

Fourth, you’ll see a weaker dollar.

When the government is eager to pay off its debt, it’ll drop the price of the dollar so it can pay back its debt in cheaper dollars.

A weak dollar equals inflated prices, which is bad for consumers because you’ll have to pay more for things, especially for imported ones.

This means you’ll see everything from your grocery bills to gas prices spike tremendously.

But even after knowing all this, you might still be wondering what this has to do with you today.

What’s the benefit of knowing any of this for you today? How does it affect your life?

The answer to that is this: it arms you with the knowledge to prepare for the future and what may be just around the corner.

After all, planning ahead is the key to any kind of success, including your financial success.

Planning Ahead

How you can prepare for the impacts of the national debt

While there’s not a whole lot you can do to change the way the government manages its finances and debt, there is something you can do to prepare for the future.

You should prepare for when the nation’s debt ends up impacting the economy—and your very own pocket.

First, do a better job of managing your own finances.

Being buried in a mountain of debt yourself when the nation is trying to get out of its own is definitely not a good idea—and it’s not a good place to be, period.

If you’re in debt and you’re not even making any headway toward paying back that debt when the government tries to get rid of its own, it’ll be an uphill battle with everything working against you.

What little money you may be saving toward paying off your debt may end up getting swallowed up by inflation, rising costs, and higher interest rates.

And to survive, you could end up having to borrow more money, and take on more debt, as a result of this.

That will only exacerbate your situation.

If you’re already headed in a direction where you will be in debt or are in debt, act today to start turning your situation around and digging yourself out of debt.

Take basic budgeting courses or read a book on personal finance to understand basic finance.

You might think it’s easy for me to say all of this. But I’m also speaking from personal experience.

When I was younger, my personal finances, including all of my student loan debt, was completely out of control.

Although they teach a lot of subjects in high school, no one’s teaching you the ins and outs of being financially responsible.

There were no discussions at our dinner table with my parents because they were both working more than one job every day to support my brothers and me.

But eventually I learned how to manage my debt, and you should too.

It’s not as difficult once you get started.

Understanding how to manage your budget and avoid overspending will not only help you get out of the hole.

It’ll also be extremely helpful to you later on in life as you seek solid financial footing.

Second, prepare for a higher cost of living in the future by tightening purse strings and only buying things you truly need.

While it’s okay to indulge every once in a while, don’t go overboard and make a habit of splurging on things you could probably do without.

Third, make sure you have enough cash on the side for a rainy day.

Savings is an important financial strategy for anyone.

But be particularly practical about saving for the future now that you know there may be a time where your income (or lack thereof) may not be able to keep up with the inflated cost of goods.

Plan ahead for large future expenses.

If you’re looking to buy a home or send your kids to college some time in the future, make sure you plan and prepare starting today.

Save up what you need and make sure you don’t frivolously squander those funds on other things.

Plan and live out those plans with an eye on the future.

Give retirement a good thought and map out a plan so you can save and retire comfortably when that time comes.

It would be disheartening to edge close to retirement only to discover that the financial landscape has changed, and you no longer have enough to meet your retirement dreams.

To make sure you’re on the right track, it’s a good idea to work with a financial advisor to come up with a solid financial plan.

Even if retirement seems like a distant thought today.

Steer clear of variable-rate credit cards, loans, mortgages, etc.

These are instruments whose rates can fluctuate, meaning the amount you pay for interest can fluctuate.

You don’t want to be stuck with a varying rate during uncertain times.

Opt for fixed rate loan options instead to remove the guesswork so you have a solid and definite idea of how much you’ll need to put toward your payments each month.

Plan for the unexpected.

People spend most comfortably when they’re doing well and feel financially secure.

In fact, that’s partially the reason why the US has a $1 trillion credit card debt.

But unexpected things can happen that can suddenly change your financial outlook.

For example, in a drowning economy, you might lose your job, or your business could tank.

It’s impossible to be fully prepared for anything, but having a backup plan for most things that could go downhill or sour, like a financial crisis, is never a bad idea.

Keeping an eye on the future

No one can fully predict what the future holds, but what we do know is the national debt can impact your wallet

That’s because when the government is in debt, it has to borrow money from other sources.

This includes investors and countries, like China and Japan, and also from government programs like Social Security.

If it comes time to pay back our debt, that means the government has to find a way to come up with that money.

Meaning it will increase taxes to get those dollars out of taxpayer’s pockets.

When and if that does happen, consumers will have to pay higher taxes, face a weaker job market, see higher interest rates and beat inflation.

These are tough changes to face if your personal financial situation is already in a dire state.

The best thing to do to protect yourself from the future effects of the national debt is to plan and save from now.

Spend cautiously and take control of your own finances to be prepared for future changes.

Learn how to budget and understand the basics of cash flow so that you can manage your money wisely.

Plan for retirement and other future expenses in advance to beat inflation.

Be better prepared for an increase in the cost of living that may result from the effects of the national debt by saving and making sure you have enough for a rainy day.

Remember, the best way to safeguard your future is to take action and maximize what you can do today.

What do you think the government should do to better manage the nation’s ballooning debt? Let us know in the comments below!