Updated: Oct 28, 2021

Freedom Debt Relief Review

Estimated read time: 15 minutes

Maybe you’ve seen their commercials on TV, "reduce your debt by up to 50% and just make one low monthly payment."

Freedom Debt Relief is a familiar presence to many people, but does it really work?

And what should you know before you consider a debt relief service?

In this detailed Freedom Debt Relief review, we’ll take a closer look behind the company and their claims, to help you decide if debt resolution is the right choice for you.

What we found may surprise you – so let’s dive right in:

The Verdict

Freedom Debt Relief does work to resolve unsecured debt, but it takes time – and results may vary

Here’s the thing about debt relief — no two consumers are alike.

The only thing they have in common is that they are simply unable to continue meeting their payment obligations (for a myriad of reasons), and have found themselves struggling to stay afloat.

When you factor in the possibility of missed payments, high interest charges, penalty APRs and other fees, trying to pay down your debt can feel like you’re spinning your wheels in the mud.

If you’ve reached this point with your debt, Freedom Debt Relief may very well be able to help you.

They do this by negotiating with your creditors to try and make your debts more manageable — but this can often come at a cost to your credit score.

Also, despite the company’s promise that users do not need to file bankruptcy, many Freedom Debt Relief customers ultimately chose to go this route anyway.

This is less of a testament to Freedom Debt Relief’s inability to perform and more of the consumer’s decision, since every user has a different debt management background and for some, bankruptcy may be the best option.

What’s more, as with all major financial undertakings, debt relief takes time — sometimes 48 months or more to complete depending on the amount you owe.

Debt resolution takes commitment and dedication – but the results can be well worth it if you’re willing to stay the course.

Why You May Need Their Services

You should use Freedom Debt Relief if you are $7,500 or more in debt

Do you have $7,500 or more credit card or store card debt?

Are you struggling with high interest rates and feeling overwhelmed as the debt builds up?

If you answered yes, then Freedom Debt Relief may be able to help negotiate reduced interest rates and help you pay off high interest cards for less than you owe.

Since its founding in 2002 by two Stanford Business School graduates, Freedom Debt Relief claims to have helped customers resolve over $2,000,000,000 (yes, two BILLION) dollars in debt.

Its founders saw that there were no truly consumer-focused, helpful debt resolution services available, so they created Freedom Debt Relief to offer services and education to those who are struggling with debt.

Many people recognize Freedom Debt Relief through their television ad campaigns, which claim to be able to reduce your debt by 50% or more.

In exchange for this high debt resolution rate, however, they are somewhat selective about the consumers they choose to work with.

In order to ascertain if Freedom Debt Relief can help, the company has each user go through a basic debt evaluation process.

This simply involves laying out how much you owe on each credit card or loan, what the interest rate is, and who the card issuer is.

With this information, your certified debt counselor can then get the full picture of your debt negotiation needs and whether or not they can help you.

Beyond the debt evaluation, Freedom Debt Relief works one on one with each customer to design a program that fits their specific needs.

Customers who have less than $7,500 in debt may be better served through a debt consolidation loan or credit counseling services.

Outlining a strategy and sticking to a debt payment time frame that works for both the customer and the companies they owe not only helps foster good financial habits, but also helps you work toward your goal of being debt-free.

What People Love About It

People love Freedom Debt Relief because of their caring, compassionate customer service and follow-up

Oftentimes, people who are overwhelmed with debt feel as if there is nowhere to turn for help and that bankruptcy is their only option.

Fortunately, Freedom Debt Relief exists as a bankruptcy alternative that has helped thousands of people get back on track while reducing how much they owe.

Here are just a few of the major reasons why people love Freedom Debt Relief:

Compassionate and caring credit counselors

Many people who use Freedom Debt Relief find that their assigned credit specialist is kind, compassionate and caring.

They remark that their specialist will often follow-up with them and help answer any questions they may have — above and beyond the debt settlement process.

Customized plan that works with the customer’s budget

Many of the reviews about Freedom Debt Relief are from people who felt they had no other options available, but through a carefully tailored and customized debt payment plan, were finally able to improve their situation and pay down their debts.

Ability to see progress through their member’s account

Users feel as if a weight has been lifted off their shoulders as they can log into their member’s account at any time and see which debts are currently being negotiated, and which are next – helping them make measurable progress toward their goals.

Needless to say, being able to shrug off the heavy burden of considerable debt is enough to make anyone feel better – owing to Freedom Debt Relief’s remarkable reviews and commitment to their customers.

Biggest Complaints

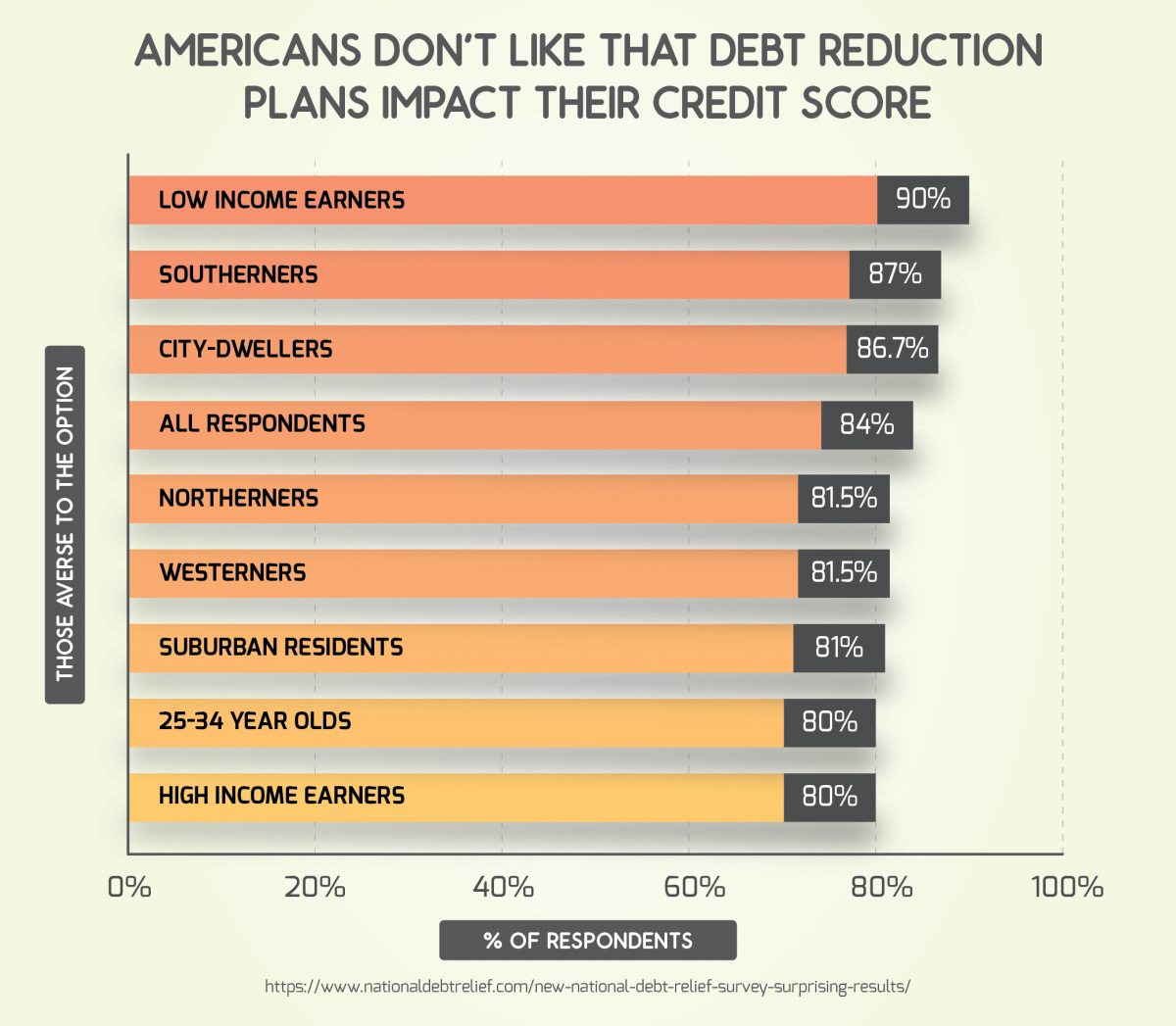

The biggest consumer complaints about Freedom Debt Relief is that enrolling in a debt resolution plan may adversely affect your credit score

Debt resolution is not an overnight process, and if you fail to follow the program that has been laid out for you, it’s more likely that you will fall back into your old spending habits.

What’s more, depending on the type of debt resolution plan you enroll in, it may severely impact your credit.

It takes too long to pay down debts

Freedom Debt Relief states from the start that it can take anywhere from 24-48 months to negotiate your debt.

This is because the company negotiates independently with your creditors. This takes time to do and some creditors are more open to negotiation than others.

A significant portion of your funds are "off limits"

While your debt is being negotiated, you’ll need to set aside around 15% or more of your funds into this separate FDIC-insured account so that Freedom Debt Relief can then negotiate a reduced payment on your behalf.

For many people, this can feel as if a chunk of their money is tied up long-term.

Keep in mind that although you own the account, the money set into it is strictly used to help pay down your debts – so that money cannot be used for any other purpose.

You may not qualify for debt relief

If you have a certain kind of debt, such as federal student loans, mortgage debt or auto loan debt, Freedom Debt Relief will not be able to help you, as these loans are generally tied to some form of collateral (your home or your car, for example), although they do help with private student loan debt on a case-by-case basis.

Freedom Debt Relief may not operate in your state

Depending on the state you live in, there may be other rules and regulations regarding how your debt can be handled. Freedom Debt Relief currently operates to varying degrees across 34 states.

To find out if your state is serviced by Freedom Debt Relief or what services are available, you are encouraged to call 1-800-544-7211 to talk with a certified debt consultant.

May severely impact your credit score

It’s a well-known fact that filing for bankruptcy will severely impact your credit score. Settling your debt for less than you owe may also considerably affect your score.

On the opposite end of the spectrum, things like credit counseling may not make much difference to lenders.

The degree to which your debt management plan affects your credit score will depend entirely on which type of plan you ultimately enroll in, so be sure you understand the end result fully before you complete the sign-up process.

The Competition

Freedom Debt Relief competes with National Debt Relief

Both of the companies have decades of experience helping consumers resolve their debt and both have similar fee structures, but there are some notable differences between them.

Fee structure of 15-25% of your total enrolled debt

Both Freedom Debt Relief and National Debt Relief have a complex fee structure that varies based on how much debt you enroll in the program with – rather than how much debt they ultimately settle with from your creditors.

This means that you may pay more for these services depending on how much you owe.

However, this is where the similarities end.

Encourage better spending and saving habits with credit counseling

Although both companies offer similar services, Freedom Debt Relief goes the extra mile to offer credit counseling services to their customers.

This not only gives you a road map to help pay down your debt, but also prevents you from accumulating more debt in the future.

Do-it-yourself options available

If you’d rather try to tackle your debt on your own, Freedom Debt Relief provides you with online tools that help you calculate your debt and form your own payment plan to track your progress.

Varying degrees of success

Owing to its selectivity, Freedom Debt Relief claims debt reductions of up to 50% compared to National Debt Relief’s average 30% debt reduction.

On the flip side, however, National Debt Relief generally is more relaxed in its acceptance of clients in various financial situations.

The Question Everyone Is Asking

Is Freedom Debt Relief a scam?

For a company to advertise a reduction in as much as half of your unsecured debt, many people understandably wonder if Freedom Debt Relief is a scam.

Consumers will be glad to know that Freedom Debt Relief is in fact a legitimate company and is a founding member of the American Fair Credit Council (AFCC) as well as a Platinum Member of the International Association of Professional Debt Arbitrators.

They also have an A+ rating from the Better Business Bureau.

Countless customer reviews can attest to the superior service and peace of mind they bring their customers – with many users lauding the professionalism, kindness and understanding shown to them by their debt management advocate.

With the underlying goal being to reduce the consumer’s debt by as much as possible in the shortest possible time while avoiding bankruptcy, it’s safe to say that Freedom Debt Relief’s decades of history and their track record show that they have lived up to this high standard.

What The Company Does

Here’s how Freedom Debt Relief works

Debt relief is known by many different names, including debt settlement, debt negotiation and debt resolution.

In short, Freedom Debt Relief is designed to help resolve your debt for less than you owe.

The first step in any debt resolution program is to set up a manageable strategy for long-term debt relief.

Here’s a closer look at the different debt solutions that Freedom Debt Relief offers:

Credit counseling

With credit counseling, you pay one monthly payment and work one-on-one with a certified credit counselor.

Here, the counselor will review your situation and, if possible, negotiate lower interest rates with your creditors.

They will also create a plan for you to follow to help you avoid getting back into debt again.

Keep in mind that this does not reduce your principal debt, and it may affect your credit report.

If you only need a straightforward plan to get out of debt, this may be an alternative solution to debt settlement.

Debt consolidation

Debt consolidation allows you to take out a single loan to repay all of your debts. You make fixed monthly payments until the debt is paid off.

One of the major benefits of debt consolidation is that the interest rate of the loan may be lower than the interest rate on your credit cards.

Because monthly payments are predictable, you can plan out your payment schedule in advance.

Debt consolidation has no impact on your credit report but there’s no reduction on the principal that you owe and you’ll need to at least have a good credit score in order to take advantage of this debt resolution program.

Cash-out refinance

A cash-out refinance requires you to own your home and be willing to work with a mortgage lender. Here, you’ll refinance your mortgage but take out extra cash beyond the balance of what you owe on your home.

You’d use that money to pay off your debts. It’s a tax-deductible interest payment and could be an alternative to help you pay down high-interest debts.

If you’re unable to pay down your debts, however, it may put you at greater risk of foreclosure, since it adds to your mortgage debt.

Debt Settlement

Debt settlement is Freedom Debt Relief’s specialty. Here, you’ll make monthly deposits into a separate bank account (that you own).

Freedom Debt Relief then negotiates with your creditors to accept less than what is owed.

The negotiated amount is then paid to the creditor until your debt is paid off.

This option provides for one low monthly payment that may be much lower than making minimum payments on high interest credit cards.

Results do vary, however and there is some impact to your credit.

You may also still continue to receive debt collection calls – however the goal of Freedom Debt Relief is to get your creditors to call them – not you.

Bankruptcy

Bankruptcy is a legal process where all of your assets are evaluated to pay off your debts.

The most common types of bankruptcy for individuals are Chapter 7 and Chapter 13.

Once the bankruptcy process is complete (generally within 3-6 months), you are relieved of the obligation to pay back your debt.

Bankruptcy severely affects your credit rate and could cause you to lose all of your credit cards.

It is also difficult to qualify for Chapter 7 bankruptcy due to new legislation changes. Although it absolves you of your debt, bankruptcy should be the very last effort to take in order to tame your debt.

Key Digital Services

The Freedom Debt Relief client dashboard makes it easy to watch the progress on your debt resolution

If you sign up with Freedom Debt Relief and pass their debt evaluation review, you’ll be able to create an account on their website which allows you to monitor each debt settlement from any device – including your tablet or smartphone.

This allows you to get an accurate picture of which debts are currently being negotiated and where they are in the negotiation process, as well as which debts are next.

Being able to actually see the resolution process in real-time as well as manage your account details, helps give you peace of mind that progress is being made toward your debt settlement.

FAQ

Is it available in all states?

Freedom Debt Relief is available in 34 states that provide debt relief services. However, due to local laws and regulations, not all services are available in all areas.

To find out what services are available (if any) in your state, call Freedom Debt Relief toll-free at 1-800-544-7211.

How long does it take for their debt settlement program?

On average, Freedom Debt Relief’s debt settlement program takes 24-48 months to complete.

This timeframe is based on the amount of debt the consumer holds and the ease with which it can be negotiated or settled with their creditors.

What debts do they help resolve with?

Freedom Debt Relief works primarily with unsecured debt — which is debt from credit cards and store-branded cards.

They may also, at their discretion, work with debt from private student loans.

They do not work with secured debt such as mortgage loan debt or car loan debt. They also do not handle debt from federal student loans.

Can they help my credit score to get better?

Different types of debt resolution will affect your credit score in various ways.

For example, simply asking for a debt settlement won’t hurt your credit, but succeeding in getting one will.

This is because the company has succeeded in allowing you to pay less than you actually owe.

Because your creditors aren’t getting all of the agreed-upon funds, it can reduce your credit score severely.

If you ultimately choose to enroll in a debt management plan with Freedom Debt Relief, you’ll need to close your credit cards and this can affect your score initially.

It’s a good idea to get a secured credit card after completing your debt management plan, as this allows you to steadily build your score back up.

How do they affect my credit?

This will depend on which type of plan you enroll in.

As you know, bankruptcy has the most severe and lasting impact on your credit report. Debt negotiation or settlement also can adversely affect your credit as much as a bankruptcy can since you are paying less to your creditors than you initially agreed.

Other debt management programs, like credit counseling and debt consolidation may have a lesser impact on your credit score depending on how much you owe and whether or not you’re able to leave old credit card accounts open after paying them off.

Your Freedom Debt Relief counselor will advise you of the best options to take for your specific needs, but be sure to educate yourself as well as to the lasting impact on your credit score – if any.

Can I cancel anytime?

Canceling the debt negotiation process can be difficult, since Freedom Debt Relief may be in the midst of working with your creditors to pay off your debt.

If you would like to cancel, please call the Client toll-free number at 1-800-655-6303 to determine the best option for ending your service.

Please note that Freedom Debt Relief does not offer a money back guarantee.

Can I monitor my results through FDR?

You can monitor your results through the Freedom Debt Relief member’s dashboard, where you’ll see which debts are currently being negotiated or settled, and which are next in line.

Where can I monitor my account and my progress?

You can monitor your account and the progress made in negotiating your debts through your Freedom Debt Relief member’s dashboard, available by logging in at freedomdebtrelief.com

Do they dispute erroneous and negative items to the companies on my behalf?

Disputing and resolving errors and negative items on your credit report is part of a credit repair process. Freedom Debt Relief does not offer this service.

What are the advantages of going with FDR?

Freedom Debt Relief is one of the most popular options for debt settlement because of their wide variety of debt settlement plans and their customer-focused approach.

With lower monthly fees and the ability to track your debt repayment progress, you can see the debt negotiation process over time as it happens.

How is FDR different from other companies in the same field?

Freedom Debt Relief offers to settle debts for up to an industry-leading 50% less than other debt management companies.

It also offers an affordable fee structure and a wide range of services that other companies do not — including credit counseling and the ability to do DIY debt management with helpful online tools.

How safe and legitimate is FDR? Is my information safe with them?

Freedom Debt Relief has been in business since 2002 and has helped thousands of users successfully negotiate their debts.

They use industry-standard security and encryption methods online, so your personal and financial data is safe at all times.

What is the guarantee for their services?

As each customer is different and there is no "one size fits all" approach to debt relief, Freedom Debt Relief has no money back guarantee for their services.

However, you are never charged until they negotiate a settlement.

Should I expect to be debt free by the time we are done?

Because each customer is different, you will receive a realistic estimate of how much debt the company will settle on your behalf when you have your free debt evaluation done.

How much in debt should I be before I seek out their services?

The company recommends that you have $7,500 or more in credit card debt in order to get the most use out of their services.

Consumers with less than this amount of debt may be better served by other debt repayment options.

Before you hit bottom, consider a debt resettlement service

Being in debt can feel overwhelming – but using the right debt settlement company can lift the heavy burden of stress off of your shoulders.

In our Freedom Debt Relief review, we found that the company has made measurable strides in making debt negotiation less of a taboo and more of a "light at the end of the tunnel" for tens of thousands of customers struggling with credit card debt.

The bottom line is that if you’ve reached the point where you need help, it’s worth turning to a company that has helped so many people turn their credit around and start making noticeable progress in digging out from a mountain of debt.

Do you use Freedom Debt Relief?

How has the company worked out for you?

Any great tips (or nightmares) to share with the rest of us?

Let us know in the comments below.