Updated: Nov 4, 2021

The Best Debt Consolidation Options for 2019

Estimated read time: 10 minutes

Debt can be a difficult cross to bear.

I personally know what it can be like dealing with multiple sources of debt while you’re trying to achieve the life you deserve.

In 2015, eight in ten Americans were in debt.

Although that number decreased in 2017, most Americans will stay in debt until they retire.

Most people think long-term debt is normal or even inevitable.

That’s the kind of attitude that leads to uncontrollable debt.

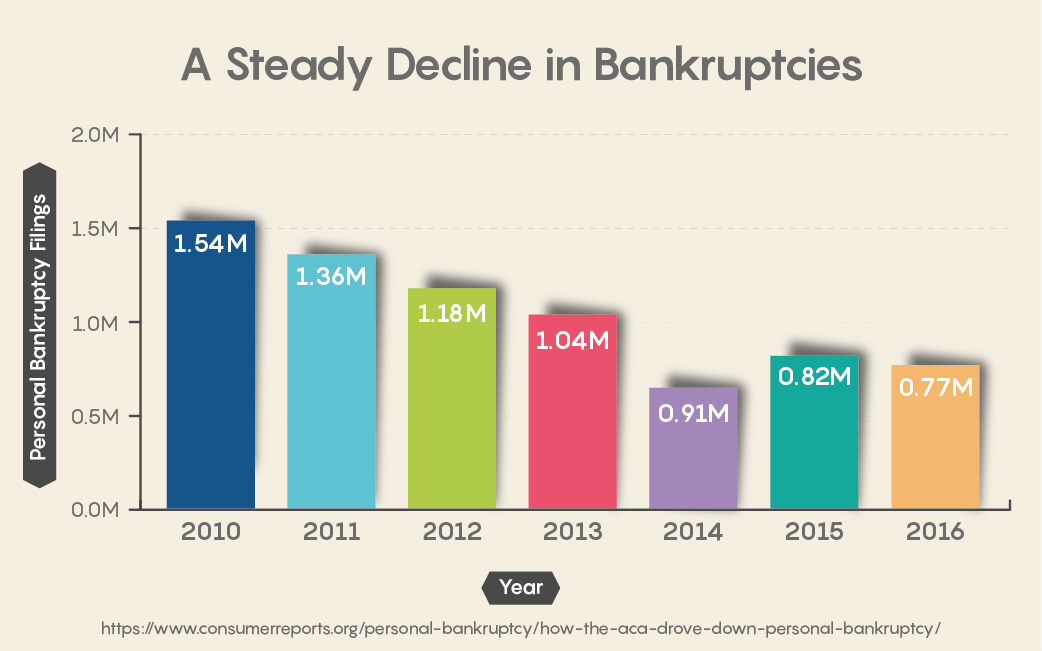

I think a lot of people believe that businesses go bankrupt more often than consumers. But it’s the opposite.

Personal bankruptcies account for 97% of all bankruptcies in the United States.

A personal bankruptcy can stay on your credit report for 10 years, and your credit score will be in shambles.

Somewhere in between developing uncontrollable debt and going bankrupt, you need to do something.

In my case, years ago my wife and I were once juggling debt.

We had several unsubsidized student loans to pay off (my wife went to law school).

In my quest to achieve my dream of running an online marketing company, I had taken out a high-interest loan.

And I was looking at having to take out another to expand my enterprise.

It was a lot to stay on top of, and I forgot to make a couple of payments on the student loans.

It was stressful.

My credit score was starting to take a beating, and I had to do something.

I did some research and made the choice to consolidate all my debts into a single loan through a home equity loan.

I borrowed enough to also support my business expansion.

I paid it all off quicker than I would have if I had kept up with minimum payments on the original debts, plus it was at a lower interest rate.

I’ve never looked back.

By putting some thought into financial planning, and making use of the tools available to you for managing and getting out of debt, you can escape the stress and agony of never-ending debt.

I’m going to help you understand the best debt consolidation options available, and the reasons why they can help set you down the path to getting out of debt.

If you’re struggling with multiple debts, consider the debt consolidation option that’s best for you and take back control of your life.

High-interest rate loans can feel like a trap. In my case, the biggest problem was the high-interest rate I was paying for my business loan.

Multiple debts are a challenge to manage. The next biggest problem was staying on top of at least four loan payments while also keeping up with credit card and other bills.

The last thing I wanted to do was add another loan to the mix, but that was what I thought I’d have to do to expand my marketing company.

Then I did some research and realized I actually had a few options to roll all of my debts into one loan, with one reasonable interest rate and one monthly payment.

Home Equity Loans

These can solve out-of-control debt by letting you borrow at a low-interest rate over a fixed amount of time

If you own your home, a home equity loan (aka, a second mortgage) can be a fantastic way to take control of debt and eventually erase it.

The solution works because home equity loans are generally lower interest than other forms of credit.

It is normal for a home equity loan to charge a little more than the interest charged on a first mortgage, for example, 4%.

Home equity loans are also structured based on a fixed term and rate, so you can plan around your one monthly payment.

It is normal for a home equity loan to be paid back in identical monthly installments over a period of 5–15 years.

Get a home equity loan is pretty easy. That’s because it is a secured debt.

You are borrowing against your home, and if you default it will be sold to pay off the lender.

When you apply for the home equity loan, the lender will run a credit check on you and will appraise your house to determine its value.

After that, you’ll get the cash you need to pay off your existing debts.

It’s as easy as that.

My story is proof home equity loans work. But if you need more proof, here’s another hypothetical example (feel free to substitute the numbers that are relevant to your personal situation).

Let’s say you have a $20,000 credit card debt. You’re being charged a 16% APR interest rate.

The minimum payment is $800 a month.

Add to that a student loan that still has $10,000 outstanding. You’re being charged 5% interest.

At a monthly payment of $188, the loan will be paid off in five years.

Finally, let’s throw in a second credit card. Maybe you had to take it out when you were unexpectedly unemployed for six months.

The balance is $10,000 and the APR is 17%. The minimum payment is $400 a month.

Here’s the home equity loan solution. You could get a five-year home equity loan at 4% interest for the full $40,000 and pay off the credit cards and student loan immediately.

Lower monthly bills and lower interest. Instead of paying a crippling combined monthly bill of $1,388, you can have a monthly bill of $736.66.

And instead of paying the existing average of 12.67% interest on the debt, you’re paying just 4%.

In five years the entire debt is gone. In the same amount of time you had planned to pay off your student loan, the entire $40,000 has been paid off with interest.

HELOC is similar, but a little different. A Home Equity Line of Credit (HELOC) is a similar option allowing you to borrow against the value of your home.

However, instead of a lump sum loan, the borrower can borrow what they need up to the determined credit limit.

Payback for a HELOC can happen at whatever schedule the borrower wants within the agreed-upon period, as long as they pay the monthly minimum.

The interest rate is variable rather than fixed.

Personal Unsecured Debt Consolidation Loans

These are another solution with lower interest rates and payments

No home? No problem. If you don’t have a home to borrow against, or if you haven’t paid enough into your home to borrow it back, you might want to look at a personal unsecured debt consolidation loan.

This debt solution is usually offered at a higher interest rate than home equity loans.

A personal unsecured debt consolidation loan interest rate of 12% would be fairly normal for a person with a "Good" credit score.

Applying for a consolidation personal loan is easier than a home equity loan. That’s because it doesn’t require an assessment of your house.

An online application for an unsecured personal loan for debt consolidation requires just a few things.

You’ll need to know the amount you want to borrow (which should be the total amounts of your existing debts).

Have your name and contact information handy.

Plus, have personal ID like your social security number and driver’s license ready.

Make sure you have all your financial information, including the source and frequency of your income, your employer information, and your bank info.

Approval can be almost instant. Usually, once you submit your information through an online application, you’ll receive approval status very quickly.

You can sign your loan documents electronically so there’s no need to wait for the mail.

Then you receive your loan as a lump sum and pay off your existing debts.

Use our calculator to figure out your ideal loan terms. As proof the debt consolidation loan solution works, you can visit our Debt Consolidation Loan calculator.

We can use it to do the math using the same hypothetical debt situation we looked at for the home equity loan.

$40,000 in total debt being charged an average of 12.66% interest (with three quarters being charged at an average of 16.5%) can be paid off immediately with a $40,000 debt consolidation personal loan.

If the debt consolidation personal loan had an interest rate of 12% and a loan period of five years, the entire debt with interest could be paid off at a monthly payment of $886.78.

That’s a lot less than the $1,388 per month that was being paid before just to make minimum payments.

Credit Card Balance Transfers

These can give you more than a year with no interest, so you can pay down the principal

If your debt woes are all about unpaid credit card balances, you might want to consider opening a balance transfer credit card.

You can take your existing balances on high-interest credit cards and transfer them to a card that’s designed for balance transfers.

Balance transfer credit cards charge 0% APR for the first year or more. Credit cards that are good for balance transfers can have anywhere from 9–21 months with an introductory 0% APR rate on the funds that were transferred.

Find a card with no balance transfer fees to save even more. Many credit cards charge 3–5% on the amount of a balance transfer.

But there are good balance transfer credit cards available that have no balance transfer fees.

Here’s the proof a balance transfer credit card can work. The two credit card debts from our hypothetical case totaled $30,000 and had an average APR of 16.5%.

Let’s say we moved those two balances over to a balance transfer credit card that charged no balance transfer fee and had an intro 0% APR of 12 months.

After that, the regular APR is 14%.

If you paid $1,200 a month (the same as the combined minimum payments on the previous two cards) the $30,000 would be paid off in 27 months and you’d save a whopping $4,792.47 in interest.

If you wanted to pay the whole transferred balance off during the 12-month promo period, you’d have to pay $2,575 a month.

That’s a high monthly payment, but it would ultimately save you $6,210.11 in interest.

Debt Settlement

These services can actually reduce the amount of debt you have to pay back

The only solution that can lower the level of debt you’re looking at. All of the previous options have focused on lowering the amount of interest you pay and helping you manage multiple debts through one strategy.

Debt settlement services, on the other hand, can actually reduce the amount of principal you have to pay back on your debt.

This is a solution you should only consider if you are in debt so deep you can’t qualify for any of the other solutions.

It’s the final solution before you’d have to declare bankruptcy.

Here’s how debt settlement works. You contact a debt settlement company and they contact your creditors on your behalf.

The debt settlement company negotiates a lower principal than what you owe and promises to pay it as a lump sum.

Getting something is better than getting nothing with lenders. When your creditors are offered proof that you are on the brink of bankruptcy, they will tend to accept a lower negotiated payment.

Then you pay into an account set up by the debt settlement company until there is enough to pay off each creditor in full.

You pay a fee to the debt settlement company but only after your settlement has been confirmed.

Better than bankruptcy. When we crunch some numbers, you can see why debt settlement is a better option than bankruptcy.

Let’s say you have that $30,000 credit card debt we were using in the previous examples.

A settlement company contacts your creditors and negotiates the $20,000 debt on the first card down to $10,000, and gets the $10,000 debt on the second card down to $5,000.

Now you have to pay $15,000 rather than $30,000, which is great.

You’ll set up a monthly payment with the debt settlement company and all those funds will be placed in an account until there is enough to pay off each negotiated lump sum.

Don’t forget the fees. Then you have to pay the fee to the debt settlement company.

If they charge you based on what you originally owed (let’s say at a rate of 15%) you will pay them $4,500.

If they charge you a higher rate (let’s say 30%) on the $15,000 they saved you, the debt settlement company fee is going to be identical ($4,500).

You’ll save $10,500 plus the interest you’d owe. So, your bottom line is that you paid $19,500 to clear a $30,000 debt.

You’ve got 4 solid options when it comes to debt consolidation

The best thing to do is look at these options covered here and consider which ones are right for you.

When I did the research, I discovered that I actually had choices over how to handle the creeping debt I was experiencing.

To recap, the best options are:

1. Borrow from your home. A home equity loan or Home Equity Line of Credit is ideal for people who can borrow against the value of what they’ve already put into their house.

It worked for me and I recommend it as a solution if you’re in a similar situation to the personal debt dilemma I described at the beginning.

2. Personal loans work to simplify debt and erase it. A debt consolidation personal loan works for people who don’t own a home or have enough equity in their home to borrow it back as a second mortgage.

You should be able to get a better interest rate and roll everything into a manageable single payment.

3. Move those high-interest balances over. A balance transfer can work for people whose main debts are high-interest credit cards.

If you can figure out a plan to pay off the balances within a 0% APR introductory period of a year or so, it’s a great option for you.

4. Reach out for a debt settlement service if it’s your only option. Debt settlement services are available for people who are so heavily in debt there is nothing left to do but negotiate a rebate.

Despite the fee, you’ll pay to the debt settlement company, you will still avoid bankruptcy and end up saving a lot.

Did one of these solutions help you solve your debt problems?

I’d love to know.

Please leave a comment sharing your experience (or nightmare) below.